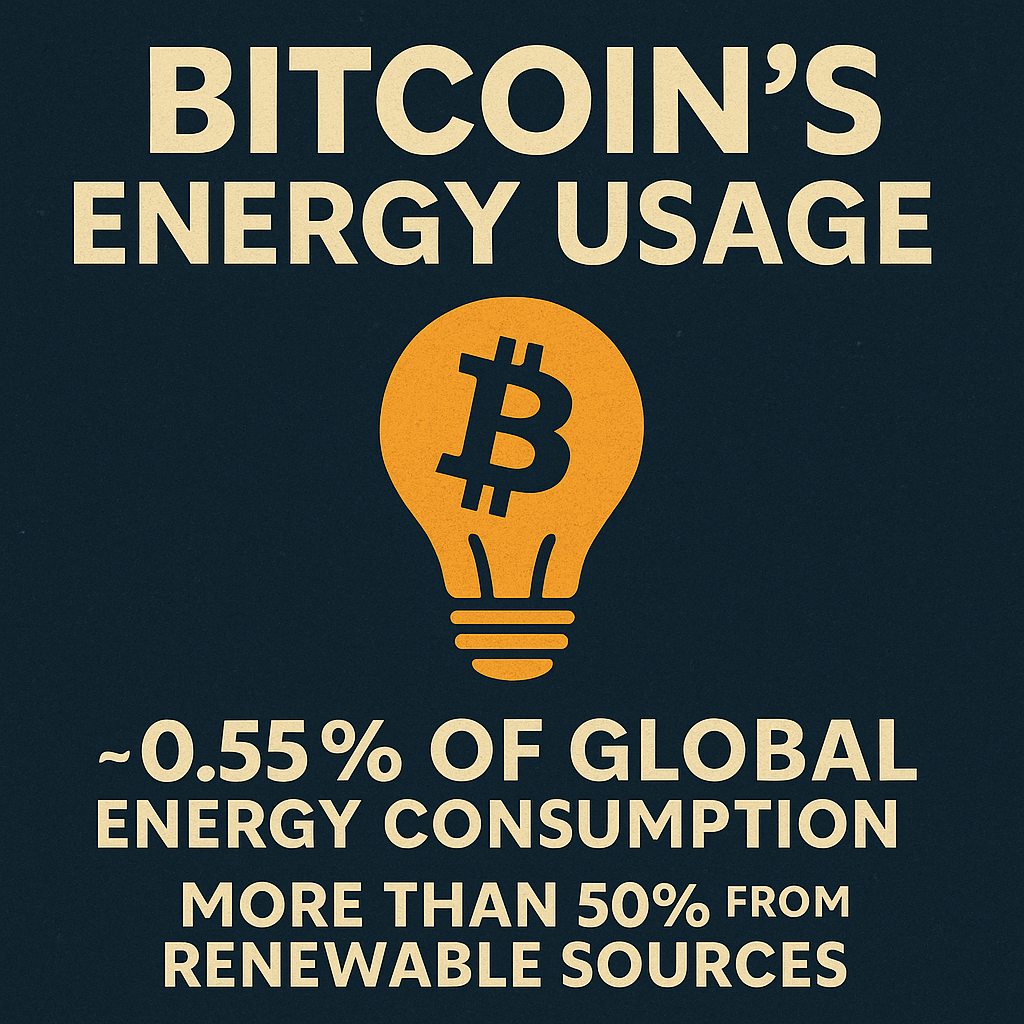

ENVIRONMENTAL CASE

for BITCOIN

ENVIRONMENTAL CASE

for Bitcoin

Explore a curated collection of articles, videos, and research that dive into Bitcoin’s environmental impact, energy use, and sustainability efforts.

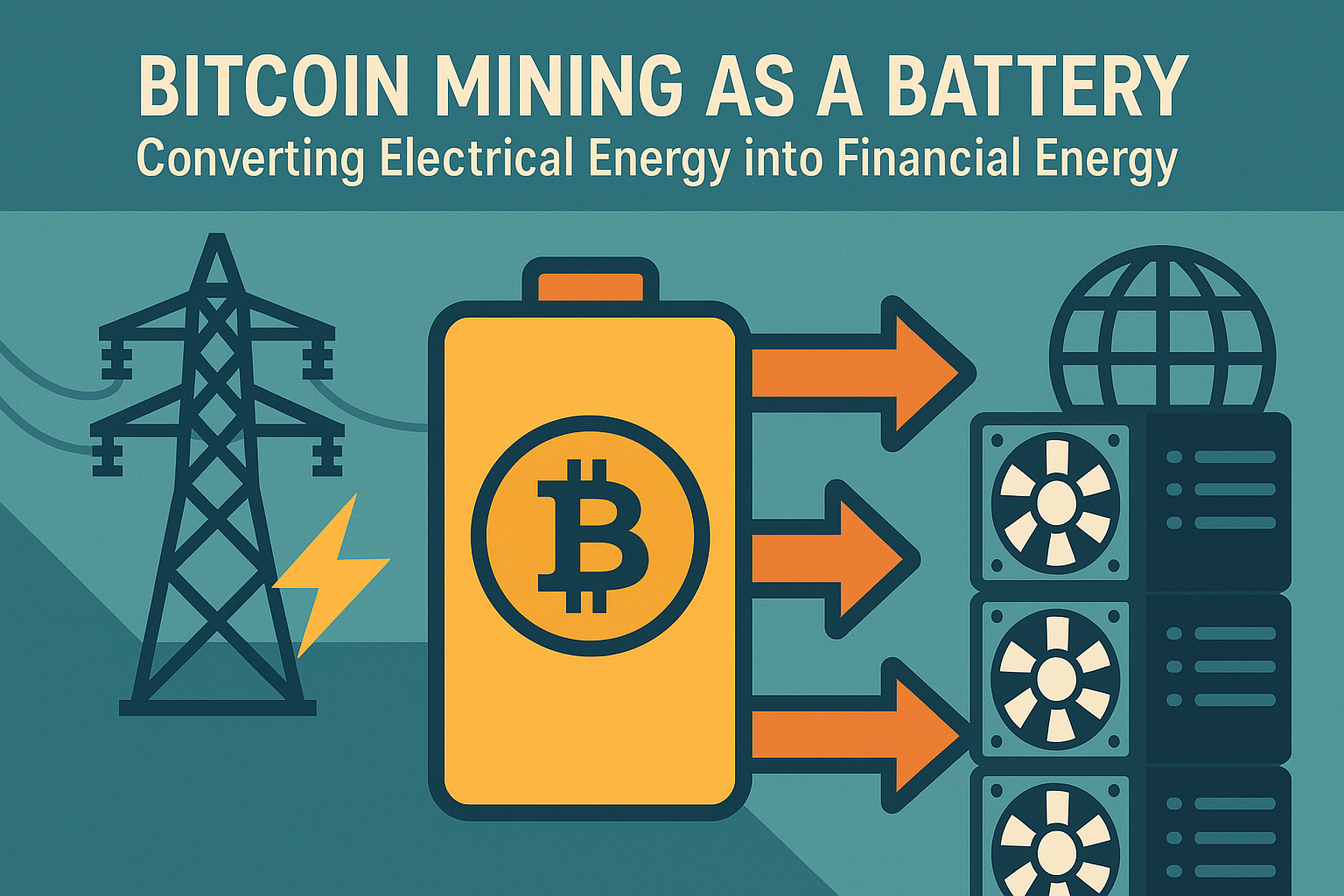

“Energy use is not a flaw of Bitcoin—it’s what gives it strength, security, and independence.”

– Lyn Alden

“Energy use is not a flaw of Bitcoin—it’s what gives it strength, security, and independence.”

– Lyn Alden

Featured

The Real Liquidity Engine Behind Bitcoin Section 2

Section 2: Stablecoins — The Rise of Synthetic Eurodollars

In the last section, we explored how offshore dollar credit acts as the hidden driver of global liquidity. But a new layer has emerged on top of that old machinery: stablecoins.

These digital tokens—denominated in dollars but issued by private companies on public blockchains—represent the latest evolution of the Eurodollar system. Where the Eurodollar extended the reach of the U.S. dollar beyond American borders, stablecoins extend it into cyberspace. They are, in effect, synthetic eurodollars, bridging traditional finance and the cryptoeconomy.

1. What Exactly Is a Stablecoin?

A stablecoin is a digital asset designed to maintain a fixed value relative to a reference currency—most commonly the U.S. dollar. The best-known examples are Tether (USDT) and USD Coin (USDC). Together, they account for more than 90 percent of global stablecoin transaction volume and serve as the primary trading pair on virtually every cryptocurrency exchange (Chainalysis, 2024) [1].

Stablecoins promise a 1:1 redemption against real dollars or equivalent reserves. To achieve this peg, issuers hold collateral—often a mix of Treasury bills, commercial paper, and cash deposits. Users can mint new stablecoins by depositing dollars (or equivalents) and can redeem them back for fiat at any time.

But here’s the critical insight: most users never redeem. Stablecoins circulate within crypto markets as digital dollars—spending months or years detached from their original collateral. In practice, they function as offshore dollar IOUs on open networks, with velocity far exceeding that of traditional bank deposits (Gorton & Zhang, 2022) [2].

2. The Eurodollar Parallel

To understand why stablecoins matter, it helps to revisit the Eurodollar analogy. The Eurodollar market began as dollar-denominated deposits held in foreign banks—outside the reach of the Federal Reserve. They were still “dollars,” but they lived offshore, unregulated, and multiplied through fractional lending.

Stablecoins follow the same pattern. They are dollar liabilities created outside the U.S. banking system, circulating in a parallel digital environment. Their issuers—Tether in the British Virgin Islands, Circle in the U.S. and Ireland, and a growing number of offshore entities—operate at the edge of regulatory oversight, echoing how Eurodollar banks once operated in London’s “shadow banking” sphere (Murau & Pflug, 2023) [3].

Just as Eurodollars allowed corporations and sovereigns to access dollar credit without going through U.S. banks, stablecoins allow global users to access dollar liquidity without touching the U.S. banking rails. For a trader in Nigeria or Turkey, holding USDT is often easier than maintaining a dollar account at a domestic bank.

The economist Perry Mehrling described Eurodollars as “money market funding of capital market lending.” Stablecoins, by comparison, could be called “crypto-market funding of digital asset trading”—the same function, updated for a new medium.

3. The Mechanics of Stablecoin Issuance

The stablecoin system can be simplified into four components:

Issuance – A user wires dollars (or equivalents) to the issuer’s custodian. In exchange, the issuer mints new tokens on a blockchain.

Circulation – Those tokens trade peer-to-peer or on exchanges, often many times over before being redeemed.

Redemption – Authorized participants (usually institutions) can burn tokens and withdraw dollars from the issuer.

Reserve Management – Issuers invest reserves in short-term Treasuries or repo markets, earning yield while users hold tokens.

This structure effectively creates money-like liabilities outside the banking system. The reserves resemble deposits, and the tokens resemble transferable deposit receipts. Yet there is no deposit insurance, no capital-reserve requirement, and no access to the Federal Reserve’s discount window.

In traditional banking, this would be called maturity transformation—borrowing short (redeemable tokens) and investing long (Treasury bills or commercial paper). When confidence falters, redemptions can trigger a “digital bank run,” as seen with the TerraUSD collapse in 2022 [4].

4. Why Stablecoins Are “Synthetic Eurodollars”

Stablecoins replicate the essential qualities of Eurodollars:

Dollar denomination outside the U.S. – Both are dollars in name but exist beyond U.S. regulatory reach.

Private issuance – Neither comes from the Federal Reserve; both are liabilities of private firms.

Dependence on confidence – Redemption promises, not physical collateral, underpin their stability.

Collateral loops – Both systems recycle reserves through money markets to generate additional yield.

Because stablecoins run on public blockchains, they add transparency and programmability missing from the original Eurodollar system. But they also inherit its fragility: opacity in reserves, exposure to interest-rate shifts, and reliance on trust in issuers (Carstens & Claessens, 2023) [5].

In essence, stablecoins are digital offshore dollars—a new species of Eurodollar that moves at internet speed.

5. The Liquidity Loop Between Stablecoins and Bitcoin

Stablecoins now dominate trading volume on crypto exchanges. Roughly 75 percent of all Bitcoin transactions are paired against USDT or USDC (Kaiko Research, 2024) [6]. This means stablecoins act as the primary liquidity conduit for Bitcoin price discovery.

When offshore dollar liquidity expands—via both traditional Eurodollar credit and stablecoin issuance—Bitcoin benefits from increased speculative capacity. When liquidity contracts, redemptions accelerate and leverage unwinds, pushing Bitcoin lower.

The correlation is not coincidence. Stablecoins inject instantaneous credit elasticity into the crypto ecosystem. Their supply expands when demand for leverage grows and contracts when traders de-risk. In other words, stablecoin issuance mirrors the same boom-and-bust dynamic that offshore dollar credit once brought to global markets (Alden, 2022) [7].

6. Regulation and Systemic Risk

Stablecoins occupy a gray zone between fintech innovation and systemic vulnerability. Regulators worry they could recreate the shadow banking risks that fueled the 2008 crisis—liquidity mismatches, opaque reserves, and contagion through money markets (Financial Stability Board, 2023) [8].

If a large issuer like Tether were forced to liquidate tens of billions of Treasury holdings rapidly to meet redemptions, it could disrupt short-term funding markets. The New York Fed has already warned that stablecoins represent a growing source of non-bank dollar creation akin to the pre-crisis repo markets (Adrian & Iyer, 2023) [9].

This underscores a key paradox: stablecoins reinforce dollar dominance even as they erode the traditional banking structure that sustains it. The more the world uses stablecoins, the more global demand for dollars grows—yet fewer of those dollars flow through regulated banks.

7. The Stablecoin–Bitcoin Feedback Loop

Stablecoins and Bitcoin have a symbiotic relationship:

Stablecoins depend on Bitcoin’s rails. Without Bitcoin’s infrastructure and credibility, early stablecoins would not have gained traction.

Bitcoin depends on stablecoins for liquidity. Most global Bitcoin trading occurs in stablecoin pairs, not fiat.

This relationship effectively ties Bitcoin’s short-term market cycles to the same global liquidity currents that govern stablecoin issuance. When Tether expands supply, liquidity enters exchanges, leverage grows, and Bitcoin rallies. When redemptions rise, the opposite occurs.

Critics often argue that unbacked or opaque stablecoin issuance artificially inflates Bitcoin’s price. While occasional abuse is possible, the broader trend is systemic: stablecoins are simply the newest mechanism through which offshore dollar liquidity enters risk markets. They are the modern counterpart to Eurodollar credit expansion—private, profit-driven, and reflexive (Bains & Bartoletti, 2023) [10].

8. The Macro Implication

Stablecoins show how the global monetary order is evolving toward programmable offshore dollars. They demonstrate that markets crave dollar liquidity so intensely that they will recreate it anywhere—whether in London in 1965 or on Ethereum in 2025.

For Bitcoin, this means its price action remains tethered (literally and figuratively) to the dollar system. Bitcoin may be apolitical money, but the liquidity denominated in dollars is what fuels its market movements. As long as the world runs on dollar credit, Bitcoin will dance to its rhythm.

In the next section, we will zoom out to examine how this struggle for trust and collateral—the bond market’s domain—is being challenged by Bitcoin’s emergence as neutral, programmable collateral in a world built on leverage.

Shout-out

For more in-depth macro and Bitcoin analysis, visit BullishBTC.com.

References (APA 7th Edition)

Chainalysis. (2024). The 2024 crypto crime and market report. https://www.chainalysis.com/reports/

Gorton, G., & Zhang, J. (2022). Stablecoins: The new wildcat banking? Yale School of Management Working Paper. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3949418

Murau, S., & Pflug, L. (2023). The new Eurodollar system: How stablecoins extend offshore dollar creation. Monetary Dialogue Report, European Parliament. https://www.europarl.europa.eu/thinktank/en/document/IPOL_IDA(2023)740026

McMillan, R. (2022). The rise and fall of TerraUSD: A cautionary tale of algorithmic stablecoins. The Wall Street Journal. https://www.wsj.com/articles/terrausd-collapse-crypto-crash

Carstens, A., & Claessens, S. (2023). The future of the international monetary system: Implications of digital money. Bank for International Settlements Bulletin No. 69. https://www.bis.org/publ/bisbull69.htm

Kaiko Research. (2024). Crypto market structure review Q2 2024. https://www.kaiko.com/research

Alden, L. (2022). Bitcoin: A global liquidity barometer. LynAlden.com. https://www.lynalden.com/bitcoin-a-global-liquidity-barometer

Financial Stability Board. (2023). Global stablecoin arrangements: Review of regulatory frameworks. https://www.fsb.org/2023/07/global-stablecoin-arrangements/

Adrian, T., & Iyer, S. (2023). Stablecoins, money markets, and financial stability. Federal Reserve Bank of New York Staff Report No. 1073. https://www.newyorkfed.org/research/staff_reports/sr1073.html

Bains, P., & Bartoletti, J. (2023). Crypto liquidity and the offshore dollar system. International Monetary Fund Working Paper 23/148. https://www.imf.org/en/Publications/WP/Issues/2023/10/02/Crypto-Liquidity-and-the-Offshore-Dollar-System-538224

Introducing Soluna’s Project Dorothy: A Wind-Powered Data Center in Texas

Bitcoin Mining: Separating Fact from Fiction

Bitcoin's Energy Consumption and its Environmental Impact

How Bitcoin Can Expand the Grid in Africa with Erik Hersman

Turning Garbage into Bitcoin with Adam Wright

Builders + Innovators Summit 2021: Crusoe Energy

OUR GOAL

Our goal is to educate others on the value of owning Bitcoin from both a financial and humanitarian perspective.

QUICK LINKS

© 2025, BullishBTC. All rights reserved.